Top Reasons Homeowners Use Their Home Equity

You’ve been paying down your mortgage and making a few upgrades, and the housing market has increased home values overall in your neighborhood. The result? You have home equity—and that’s really valuable.

Home equity is the difference between what your property is worth on the market and what you still owe on your mortgage. Over time, equity grows as you pay down your home loan or as your home gains value. Many homeowners don’t realize that equity isn’t just a number on paper. It can be unlocked and used as a tool to reach financial goals.

Whether you dream of a new kitchen, want to knock out high-interest debt, or need a cushion for life’s curveballs, your home equity could be the key. The question is: How do you access that equity and put it to work wisely? Let’s take a look.

The Benefits of Home Equity

Equity often represents one of the biggest assets a household has. In fact, U.S. homeowners are sitting on over $35 trillion in home equity. And unlike investments that may swing with the markets, equity usually builds steadily over time as you pay down your loan and as property values rise. Accessing it gives you the flexibility to:

- Fund significant expenses without relying on costly credit cards

- Simplify your financial life by rolling high-interest revolving debts into one payment

- Plan for education or other milestones

How to Access Your Home Equity

So, how do you actually turn that growing equity into cash you can use? Homeowners have a few main options, each with its own benefits:

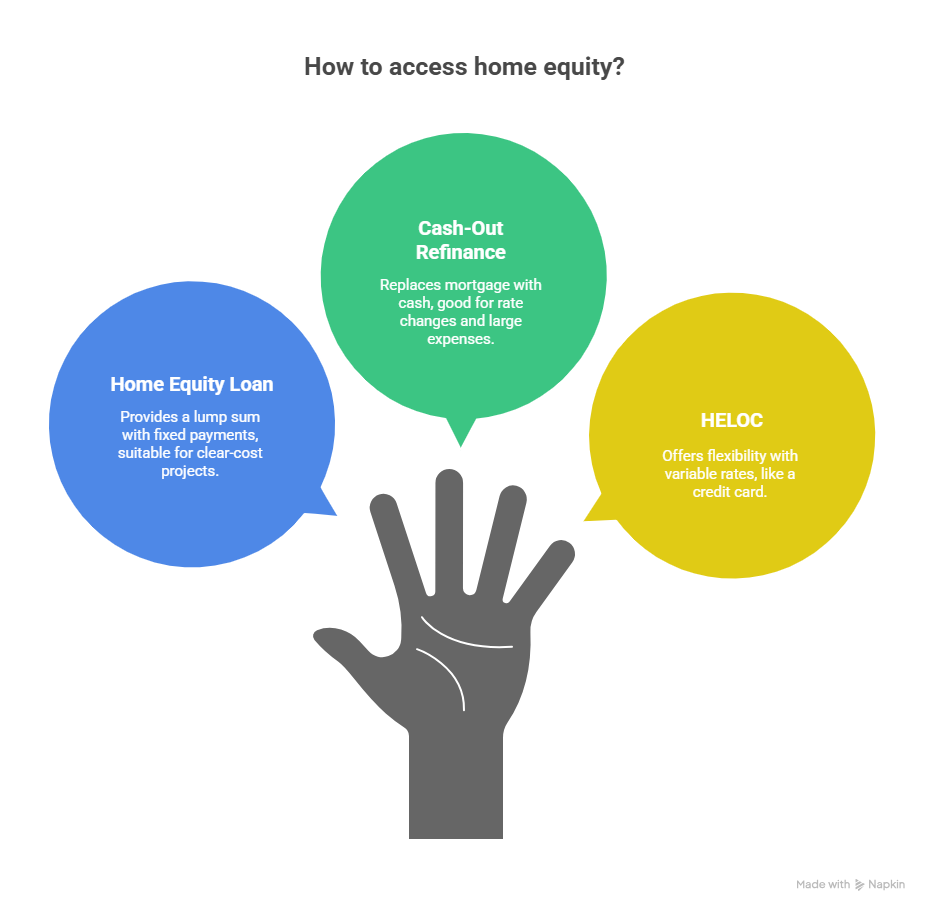

- Home equity loan. Think of this as a second mortgage that gives you a lump sum up front. You’ll repay it over a set term with fixed monthly installments, making payments predictable and easy to budget for. Home equity loans can suit projects or expenses with relatively clear costs, like a remodel, tuition or debt consolidation.

- Cash-out refinance. With this option, you replace your current mortgage with a new, larger one. You use part of the new loan to pay off what you already owe, and the rest comes back to you as cash at closing. It can be a good fit if you want to refinance for a new rate or term while also freeing up funds for larger expenses.

- Home equity line of credit (HELOC). A HELOC acts more like a credit card tied to your home’s value. You can borrow as needed during a set draw period, repay and borrow again. While it offers flexibility, the rates are often variable, which means payments can change over time.

How People Put Their Home Equity to Use

So how do homeowners actually use those home equity dollars? Here are some of the most popular ways:

Improve Your Home

One of the most common uses of home equity is updating or upgrading a property, such as replacing a roof, remodeling a dated kitchen, adding an extension or installing energy-efficient windows. These projects improve comfort and daily living, and, in many cases, they can boost the home’s resale value. A home equity loan or cash-out refinance is often well-suited for projects with a specific cost and timeline, since you receive a lump sum of funds.

Consolidate Debt

Carrying multiple high-interest debts, such as credit cards or personal loans, can be stressful and expensive. A home equity loan or cash-out refinance can consolidate those balances into one payment at a potentially lower interest rate. This can reduce the total cost of borrowing and help simplify your monthly budget. The caveat: Discipline is essential. Paying down old debt only to accumulate new balances defeats the purpose.

Pay for Education

From college tuition to private school fees, education is a major financial investment. Tapping equity through a lump-sum loan can sometimes be cheaper than certain student loans, helping families manage costs with more predictable payments.

Build an Emergency Safety Net

Unexpected events happen. Sudden home repairs, a medical emergency or a temporary job loss can all create financial strain. When savings fall short, home equity can serve as a backup source of funds, offering a cushion that brings peace of mind.

Explore New Ventures

Some homeowners use equity as seed money for a business or to purchase another property. When used thoughtfully, this can potentially open the door to new income streams and long-term growth opportunities.

Balancing Benefits and Risks

Home equity loans, cash-out refinances, and HELOCs have lots of advantages, but it’s important to use them wisely. Here are a few things to keep in mind:

- Limited equity. Every dollar you borrow reduces the ownership share you’ve built in your home.

- Market shifts. If you borrow a significant amount and property values dip, you could owe more than your home is worth.

- Tax changes. Depending on where you live, higher property values may lead to higher assessments, which can raise your property taxes.

- Upfront costs. Home equity loans, cash-out refinances, and HELOCs usually come with fees and closing costs that can add to your total expense.

- Collateral risk. If you can’t repay what you borrow, you risk foreclosure and could lose your home.

- Conservative borrowing. Use equity for needs or improvements that add lasting value, and keep some in reserve in case the housing market cools.

What to Do Before Using Home Equity

Knowing you have equity is one thing, but deciding whether to use it (and how) is another. The steps below can help you weigh your options and move ahead when it makes the most sense.

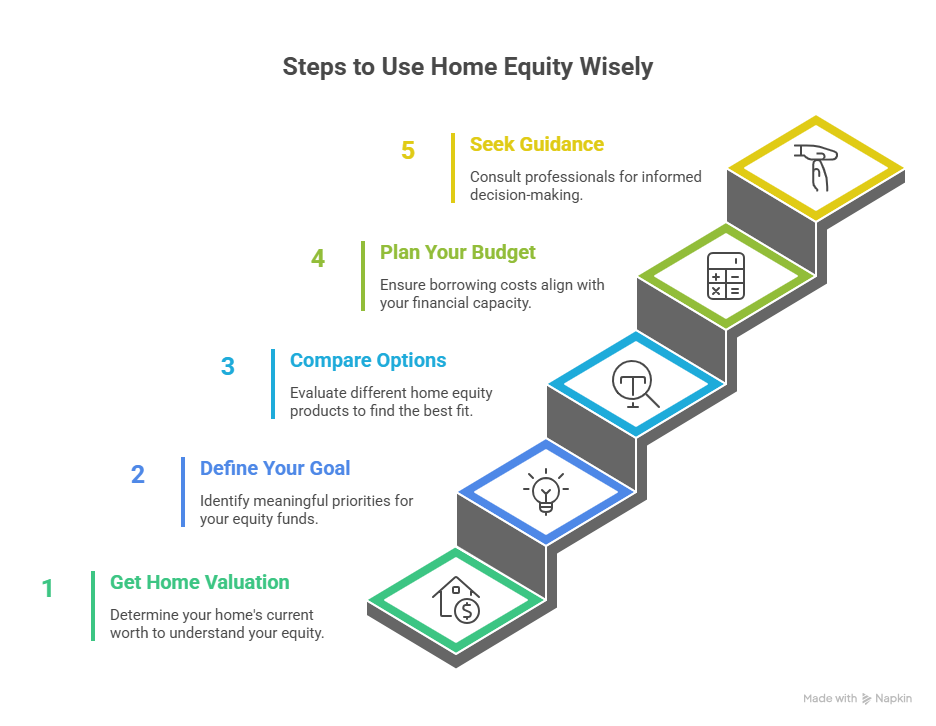

Step 1: Get an Updated Home Valuation

Start by understanding how much your home is worth today. An appraisal, a market analysis or even an online estimate can give you a ballpark figure. Subtract what you still owe on your mortgage, and you’ll know how much equity you have to work with.

Step 2: Define Your Goal

Funds drawn from your equity are most effective when applied to meaningful priorities. Focus on essentials that add long-term value, such as repairs, renovations, education, or paying off high-interest debt.

Step 3: Compare Your Options

Home equity products vary in how they’re structured. Home equity loans give you a lump sum, cash-out refinancing replaces your mortgage with a larger one, and HELOCs offer revolving credit. Look at the pros and cons of each against your needs.

Step 4: Plan Your Budget

Run the numbers to see how borrowing will change your costs. Whether it’s a new loan payment or a higher balance from a cash-out refinance, confirm the monthly amount and overall costs fit comfortably in your budget.

Step 5: Seek Guidance

Not sure which is the best home equity product for you? A trusted lender or financial advisor can walk you through the details, answer questions, and help ensure the option you choose aligns with your financial goals.

Use Home Equity to Support Your Goals

The equity you’ve built can support immediate priorities as well as long-term goals. Whether through a home equity loan, a cash-out refinance, or a HELOC, home equity products give you practical ways to meet today’s financial demands while setting you up for what’s next.