What Is Note Seasoning and Should You Wait for It?

When you’re new to the mortgage note world, you’ll come across terms that sound a little… confusing. One of those is note seasoning. It might sound like something to spice up your paperwork, but it's a very real and important part of how mortgage notes are valued and traded. If you’re thinking about selling or buying a mortgage note, seasoning plays a bigger role than you might expect. Let’s break it all down in plain language and help you decide whether waiting for note seasoning is worth your time or not.

Breaking Down the Term Seasoning

In mortgage note investing, seasoning refers to the amount of time that a borrower has been consistently making payments on the loan. Think of it like this: just as food needs time to absorb flavors and develop richness, a note needs time to show that the borrower is reliable and the loan is stable.

Typically, a note is considered seasoned once the borrower has made six or more on-time monthly payments. Some investors prefer notes with even more history, 12 months or longer, because it reduces risk and gives a clearer payment pattern. The more time passes with good payment behavior, the more seasoned the note becomes.

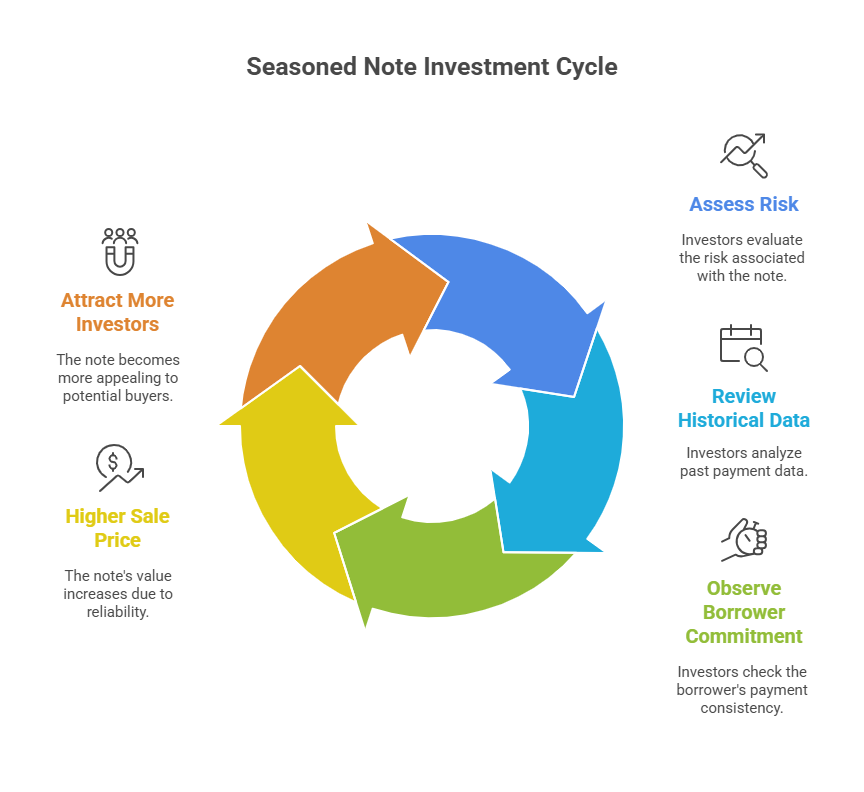

Investor Interest and Risk Comfort

From the investor’s point of view, seasoning is like a test drive. A newly originated note (also called a green note) doesn’t offer any proof that the borrower is reliable. But once you’ve got several months of steady payments, it paints a picture of a dependable payer.

Investors prefer seasoned notes because:

- They can better assess the risk.

- There’s historical data to review.

- It shows borrower commitment.

- The note may command a higher sale price.

In short, a seasoned note often feels safer to purchase, and that makes it more attractive.

Value Shifts Based on Payment History

Let’s say you’re holding a newly created mortgage note and considering selling it. If there’s little to no seasoning, you might have to sell it at a discount even if the terms look strong. That’s because potential buyers are taking on more risk without any real proof of repayment.

Now take the same note, but this time it has nine months of consistent payments under its belt. Suddenly, the value goes up. Why? Because the payment history reduces uncertainty. Buyers are more confident and often willing to pay closer to the full note value.

That said, seasoning isn’t the only factor. Things like interest rate, property type, borrower credit, and down payment size also play into what a note is worth.

.jpg)

Waiting Versus Acting Fast

This is a personal decision that depends on your goals. If you need cash quickly, waiting six to twelve months may not be realistic. But if your goal is to maximize profit and you’re not in a rush, it might be worth letting the note season.

Waiting for seasoning is generally a good idea if you want top dollar, but life and business don’t always wait for perfect conditions.

When New Notes Can Still Win Buyers

Not every buyer is afraid of unseasoned notes. Some investors specialize in these types of deals. They might negotiate a lower price to compensate for the added risk, but for sellers who can’t or don’t want to wait, this offers a path forward.

Also, buyers who have strong underwriting skills or know the borrower personally may be more willing to Buy Mortgage Note even without full seasoning. That’s why marketing your note properly and telling its full story is key, seasoned or not.

Smart Steps to Strengthen Seasoning

If you do decide to let your note season before selling, there are a few smart things you can do in the meantime:

- Document Everything: Keep a clear record of every payment, communication, and escrow detail.

- Use a Loan Servicer: Third-party servicing companies add professionalism and credibility.

- Avoid Late Payments: Work with the borrower to ensure timely payments and avoid defaults.

- Keep the Property Insured: Active homeowners insurance is a big plus for future buyers.

The more care you put into managing the note, the more appealing it will be later on.

Key Takeaways Before You Sell

Seasoning isn’t everything, but it can make a big difference in the note resale world. It helps reduce risk for buyers and gives sellers a stronger position when negotiating price. That said, waiting isn’t always necessary, if the note is well-structured or the seller has other motivations.

If you're holding a note now and wondering what to do next, think about your goals, your timeline, and how strong your borrower’s payment history is shaping up. That will give you the best clue as to whether seasoning is worth the wait or just a nice bonus.

Growing Interest in Secondary Markets

More real estate investors are tapping into the secondary note market, where seasoned and unseasoned notes change hands frequently. This growing ecosystem has created more opportunities for sellers to find interested buyers, regardless of seasoning status.

Because of this shift, note holders don’t always need to rely on traditional channels or wait for a perfect payment track record. With the right outreach or broker, selling earlier can still work out well.

.webp)